" height="7.1149px" id="FTcukYt9G" width="2.46918px"/><path d="M 14.664 0 L 8.602 6.334 L 2.49 12.662 L 2.469 12.683 L 2.469 17.111 L 0 17.111 L 0 12.14 L 3.545 8.472 L 11.85 0 Z" fill="rgb(255, 255, 255)" height="17.111px" id="JEclOrOlY" width="14.6641px"/><path d="M 8.295 6.23 L 5.406 6.23 L 0 0 L 3.097 0 Z" fill="rgb(255, 255, 255)" height="6.230199999999998px" id="A32Do9AoF" transform="translate(6.839 10.88)" width="8.29483px"/><path d="M 9.924 1.295 C 8.952 0.432 7.57 0 5.776 0 C 4.739 0 3.748 0.143 2.801 0.428 C 1.854 0.713 1.044 1.125 0.369 1.662 L 1.357 3.422 C 1.867 2.998 2.492 2.66 3.233 2.407 C 3.974 2.155 4.731 2.029 5.505 2.029 C 6.673 2.029 7.55 2.301 8.134 2.847 C 8.718 3.393 9.01 4.164 9.01 5.157 L 9.01 5.622 L 5.258 5.622 C 3.958 5.622 2.925 5.793 2.16 6.135 C 1.394 6.477 0.843 6.934 0.505 7.504 C 0.168 8.075 0 8.71 0 9.41 C 0 10.11 0.197 10.8 0.592 11.378 C 0.987 11.957 1.551 12.409 2.283 12.735 C 3.015 13.061 3.867 13.224 4.838 13.224 C 6.039 13.224 7.035 13 7.825 12.552 C 8.379 12.238 8.815 11.846 9.134 11.377 L 9.134 13.077 L 11.381 13.077 L 11.381 5.255 C 11.381 3.479 10.895 2.16 9.924 1.295 Z M 7.566 10.829 C 6.899 11.22 6.122 11.416 5.233 11.416 C 4.344 11.416 3.62 11.225 3.11 10.841 C 2.6 10.458 2.345 9.949 2.345 9.313 C 2.345 8.76 2.55 8.286 2.962 7.896 C 3.373 7.504 4.172 7.309 5.356 7.309 L 9.01 7.309 L 9.01 9.118 C 8.713 9.868 8.233 10.437 7.566 10.829 Z" fill="rgb(255, 255, 255)" height="13.223630000000002px" id="VocEMLWwR" transform="translate(15.084 4.033)" width="11.380799999999999px"/><path d="M 14.367 0 L 8.023 14.251 C 7.645 15.163 7.221 15.88 6.752 16.402 C 6.283 16.924 5.768 17.295 5.209 17.515 C 4.649 17.734 4.032 17.845 3.358 17.845 C 2.732 17.845 2.123 17.743 1.53 17.54 C 0.938 17.335 0.428 17.039 0 16.647 L 1.012 14.887 C 1.341 15.197 1.703 15.433 2.098 15.596 C 2.493 15.759 2.913 15.841 3.358 15.841 C 3.934 15.841 4.411 15.694 4.79 15.401 C 5.168 15.107 5.521 14.586 5.851 13.836 L 6.267 12.924 L 0.493 0.001 L 2.962 0.001 L 7.526 10.355 L 12.047 0.001 Z" fill="rgb(255, 255, 255)" height="17.84464px" id="tBjxqkJt3" transform="translate(26.835 4.155)" width="14.367299999999997px"/><path d="M 9.924 1.295 C 8.952 0.432 7.57 0 5.776 0 C 4.739 0 3.748 0.143 2.802 0.428 C 1.855 0.713 1.044 1.125 0.37 1.662 L 1.357 3.422 C 1.867 2.998 2.492 2.66 3.233 2.407 C 3.974 2.155 4.731 2.029 5.505 2.029 C 6.673 2.029 7.55 2.301 8.134 2.847 C 8.718 3.393 9.01 4.164 9.01 5.157 L 9.01 5.622 L 5.258 5.622 C 3.958 5.622 2.925 5.793 2.16 6.135 C 1.394 6.477 0.843 6.934 0.506 7.504 C 0.168 8.075 0 8.71 0 9.41 C 0 10.11 0.197 10.8 0.592 11.378 C 0.987 11.957 1.551 12.409 2.283 12.735 C 3.015 13.061 3.867 13.224 4.838 13.224 C 6.04 13.224 7.035 13 7.826 12.552 C 8.379 12.238 8.815 11.846 9.134 11.377 L 9.134 13.077 L 11.38 13.077 L 11.38 5.255 C 11.38 3.479 10.895 2.16 9.924 1.295 Z M 7.566 10.829 C 6.899 11.22 6.122 11.416 5.233 11.416 C 4.344 11.416 3.62 11.225 3.11 10.841 C 2.6 10.458 2.345 9.949 2.345 9.313 C 2.345 8.76 2.55 8.286 2.962 7.896 C 3.373 7.504 4.172 7.309 5.356 7.309 L 9.01 7.309 L 9.01 9.118 C 8.713 9.868 8.233 10.437 7.566 10.829 Z" fill="rgb(255, 255, 255)" height="13.223630000000002px" id="CzZaw0etF" transform="translate(41.005 4.033)" width="11.380300000000005px"/><path d="M 14.083 12.754 L 3.687 12.754 L 1.408 17.749 L 0 17.749 L 8.245 0 L 9.551 0 L 17.796 17.748 L 16.388 17.748 Z M 13.597 11.663 L 8.885 1.42 L 4.2 11.663 Z" fill="rgb(255, 255, 255)" height="17.7487px" id="Q9MGA6hKQ" transform="translate(58.083 0)" width="17.795900000000003px"/><path d="M 0 0 L 1.306 0 L 1.306 17.748 L 0 17.748 Z" fill="rgb(255, 255, 255)" height="17.7482px" id="y1_76E5id" transform="translate(79.132 0)" width="1.3057000000000016px"/></g></svg>)

AI demand is still rising. The harder question is whether America can build the infrastructure quickly enough, and with enough local consent, to meet it.

The most important signal in the U.S. data center market may no longer be another hyperscale campus announcement. It may be the growing number of communities trying to slow, restrict or block those projects before they are built.

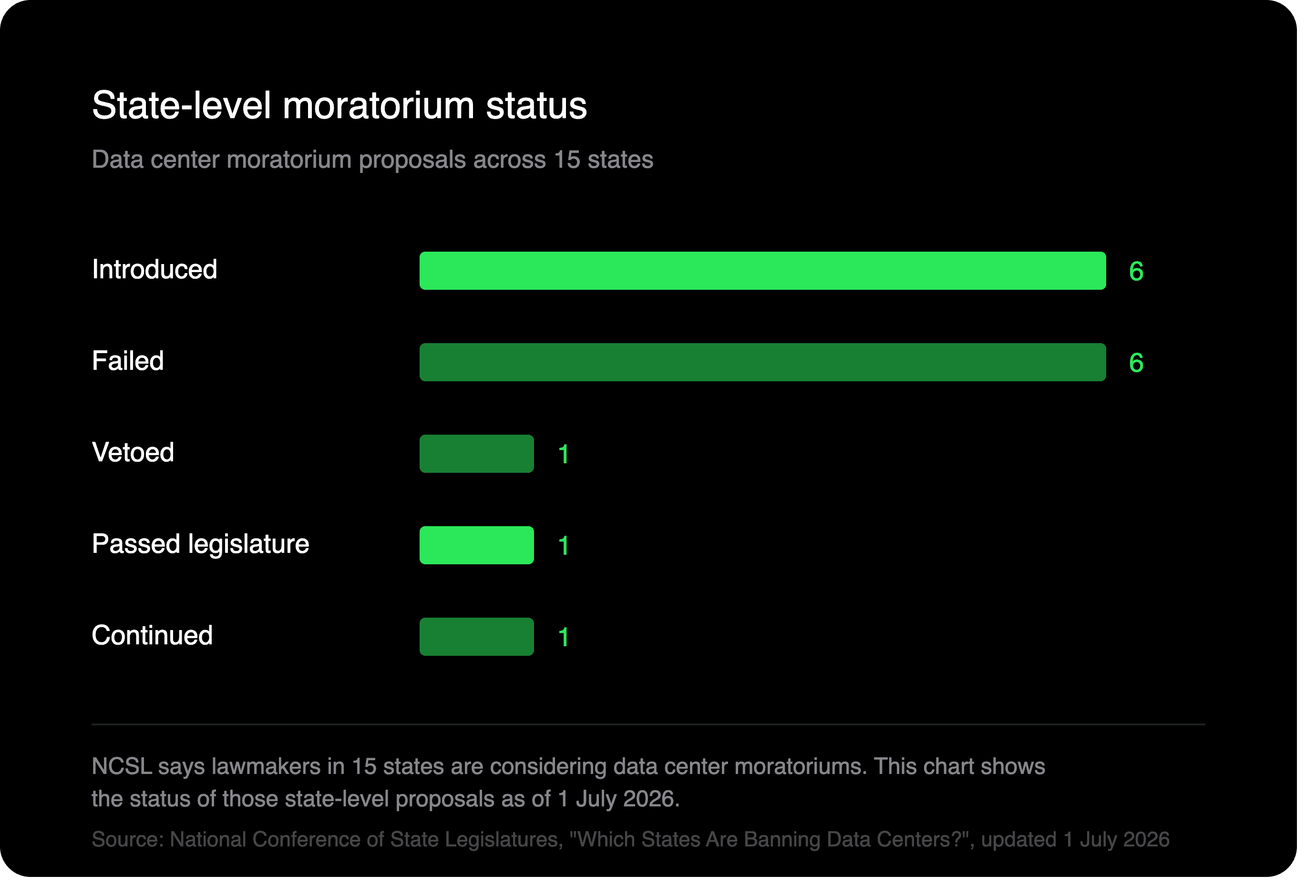

More than 300 bans and moratoriums are threatening the U.S. data center boom. The public state-level data points in the same direction. NCSL says lawmakers in 15 states are considering data center moratoriums, while DataCenterBans.com’s tracker lists 19 of 50 states as restricting or considering restrictions. These figures do not mean 300 projects have been cancelled. They do mean the industry’s assumed path from announced capacity to delivered capacity is becoming more contested.

NCSL says lawmakers in 15 states are considering data center moratoriums. This chart shows the status of those state-level proposals as of 1 July 2026.

Source: National Conference of State Legislatures, “Which States Are Banning Data Centers?”, updated 1 July 2026.

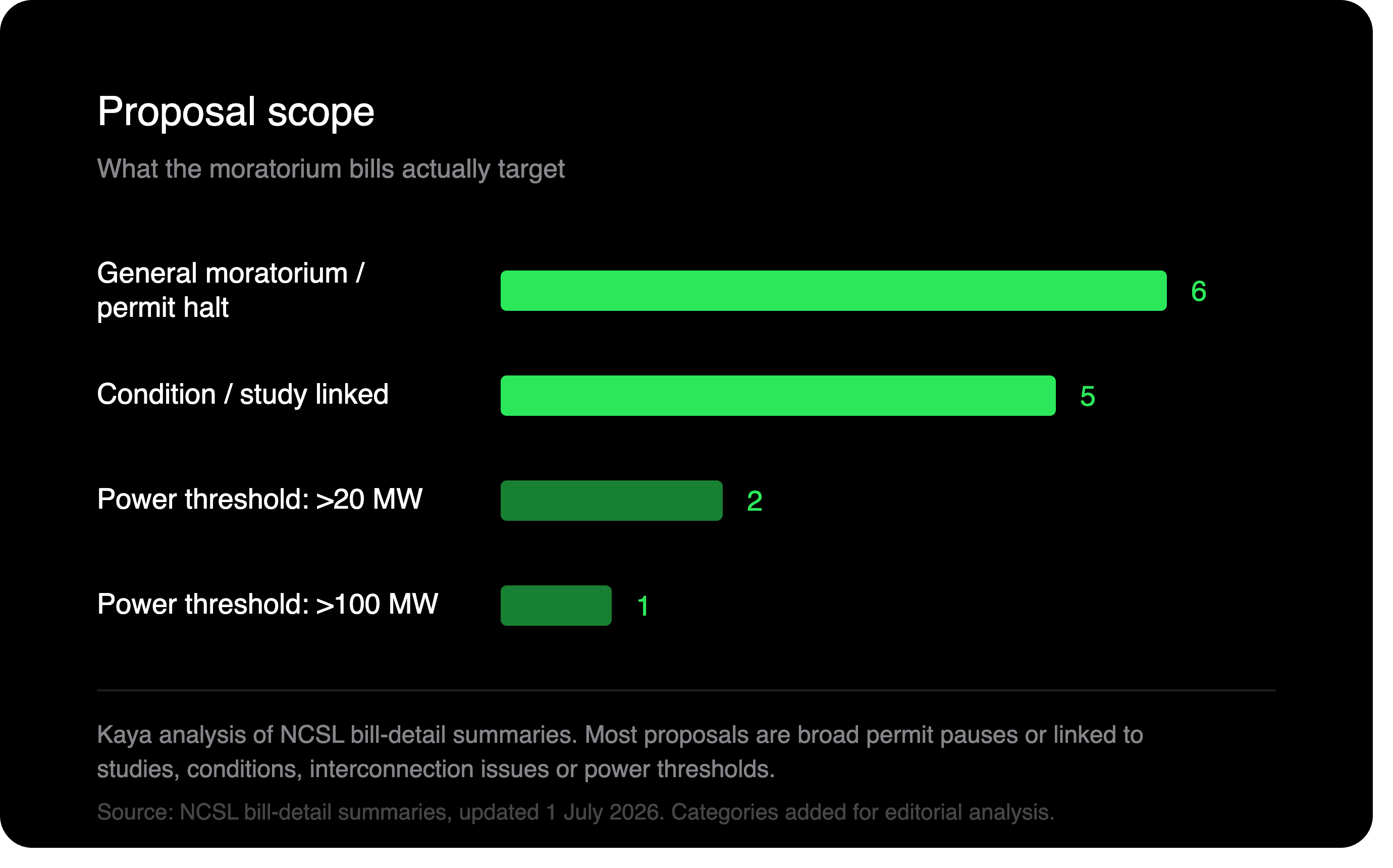

Kaya analysis of NCSL bill-detail summaries. Most proposals are broad permit pauses or linked to studies, conditions, interconnection issues or power thresholds.

Source: NCSL bill-detail summaries, updated 1 July 2026. Categories added for editorial analysis.

NCSL’s state-level table shows how data center moratorium proposals vary by state, status and scope.

Source: National Conference of State Legislatures, updated 1 July 2026.

That distinction matters. The data center boom is real. Demand for AI compute, cloud capacity and low-latency infrastructure remains strong. Capital is still flowing. The problem is that demand and capital do not automatically produce buildable sites, energized facilities or politically durable projects.

A new constraint is emerging: permission.

For owners, developers, program leaders, contractors and capital committees, the implication is uncomfortable. The next phase of the data center boom will not be won by the groups that announce the most capacity. It will be won by the teams that can prove deliverability earliest, across power, water, land use, permitting, procurement, construction readiness and local trust.

The gap between announced capacity and buildable capacity

The data center industry has spent the past two years speaking in increasingly large numbers: gigawatts, billions of dollars, millions of square feet, and entire regional campuses designed around AI workloads.

Those numbers tell only part of the story.

A data center campus is not a software deployment. It is a physical infrastructure program. It requires land, transmission, substations, transformers, switchgear, cooling systems, backup power, fibre, skilled labour, commissioning teams and local approvals. If any one of those components slips, the whole program can move out of sequence.

The Blackstone-backed QTS Digital Gateway project in Prince William County, Virginia, has become a useful warning. The proposed campus had secured local rezoning approval and was expected to become one of the world’s largest data center developments. It was later terminated after sustained local opposition, litigation and a court ruling tied to public notice requirements.

The project’s collapse showed that approval can be fragile. A site may look viable in an investment memo, in a zoning vote or in a development pipeline. Yet its deliverability can still be undone by legal process, community pressure or procedural failure.

For those accountable for portfolio delivery, this is the market’s new risk premium. A project cannot be described as shovel-ready until it has survived the local, legal, power and public-permission tests that increasingly determine whether construction can proceed.

Why the opposition is hardening

It is easy for the industry to dismiss local resistance as NIMBYism. That is too simple.

Many communities are responding to a perceived imbalance between the local costs of data center development and the local benefits. Residents see projects that could reshape electricity demand, water use, land value, traffic, noise and public infrastructure. They are less easily persuaded by abstract promises about national AI competitiveness or future digital growth.

The concerns are often practical. Who pays for grid upgrades if a campus requires new transmission or substations? Will residential customers carry part of the cost through higher utility bills? How much water will the facility use directly, and how much water is consumed indirectly through power generation? What happens to agricultural land, local roads and neighborhood noise levels? How many permanent jobs will be created after construction ends? What tax incentives were offered, and who negotiated them?

Those questions are becoming more difficult to answer with conventional economic-development language.

Data centers can generate substantial tax revenue in the right fiscal structure. Loudoun County in Virginia remains the most cited example. But Loudoun is an outlier. Its tax base, data center density and personal property tax model are not easily replicated. In many other markets, the financial case is less straightforward, particularly where developers receive tax abatements while communities absorb visible infrastructure burdens.

The economics are therefore becoming political. Communities are asking whether they are hosting a strategic national asset or underwriting a private industrial load.

Power is now a public issue

Power has become the central constraint in data center development. It is also becoming a public-permission issue.

AI workloads require a level of electricity demand that can change the planning assumptions of regional grids. Large campuses can require dedicated substations, transmission upgrades, new generation or behind-the-meter power. These are not small changes to the local infrastructure base.

The cost question is politically sensitive. Utilities have historically recovered infrastructure costs through regulated rate structures. Where upgrades are linked to large new loads, residents and policymakers are increasingly asking whether ordinary customers should subsidize the power requirements of highly profitable technology companies.

That debate is already shaping policy. Several states have considered measures to protect residential ratepayers from data-center-driven grid costs. Oregon’s large-load rate actions and proposed ratepayer protections in states such as Georgia show how energy policy is becoming part of the data center approval process.

For project sponsors and delivery leaders, this changes the power conversation. It is no longer sufficient to say a project has requested capacity or entered an interconnection queue. Local officials and residents will increasingly want to know how that power will be supplied, who will pay for the infrastructure, how reliability will be protected and whether the project will push costs onto the wider community.

Power strategy has become part of the license to build.

Water, noise and the local footprint

Water is becoming the other major flashpoint.

The debate is no longer limited to the volume of water used for cooling. It now includes indirect water use linked to electricity generation, wastewater discharge, commissioning processes and the capacity of local treatment systems. In drought-prone or agriculturally sensitive regions, even a technically efficient cooling plan can face resistance if communities do not trust the numbers or the process.

Noise has also become a more serious risk. High-density AI facilities can require significant cooling and backup systems. When acoustic modelling proves inadequate, residents experience the project as a permanent industrial intrusion rather than distant digital infrastructure.

These issues shape litigation risk, permitting risk and local political durability. They also affect design, procurement and scheduling decisions. A project that must change its cooling strategy, acoustic mitigation or water plan after public backlash can quickly lose months.

The physical externalities of compute are becoming harder to obscure.

The procurement consequence

Bans and moratoriums may look like political stories. For delivery organizations, they are schedule, procurement and capital-allocation risks.

Hyperscale data centers depend on long-lead electrical and mechanical equipment ordered well before a site is fully built. Transformers, switchgear, generators, cooling systems and specialized components must be procured on timelines that often run ahead of final local certainty.

That sequence is becoming more dangerous.

If a moratorium pauses rezoning, a lawsuit voids approval, a water ordinance changes cooling requirements, or an interconnection study slips, the project supply chain can fall out of alignment with the legal right to build. Equipment may be ordered for a site whose schedule has moved. Field teams may be planned around energisation assumptions that are no longer credible. Capital may be committed before public-permission risk has been resolved.

This is where the data center boom becomes an operating-model problem for anyone carrying delivery accountability. Boards and program teams cannot manage a permission-constrained buildout with fragmented visibility across site selection, permitting, utility coordination, procurement, logistics and field execution.

The risk is no longer contained inside one workstream. It moves across the whole project.

The power-plus-permission era

The first phase of the AI data center boom rewarded speed, land aggregation and access to power. The next phase will reward proof.

Proof of firm power. Proof of credible water strategy. Proof of community engagement. Proof of durable approvals. Proof that economic benefits are meaningful at the local level. Proof that long-lead procurement is aligned with real project readiness.

This is the power-plus-permission era.

In this environment, speculative capacity will become less valuable than deliverable capacity. Investors will start to distinguish between projects with public announcements and projects with a credible path through power, policy, permitting and construction.

That shift will matter to owners and contractors as much as developers. A site’s real status will depend on more than design maturity or procurement progress. It will depend on whether the upstream risks that can stop construction have been identified early enough to manage.

The industry lesson

The U.S. data center boom is not ending. But it is becoming more selective.

The presence of more than 300 local restrictions does not mean communities are rejecting AI infrastructure altogether. It means the terms of acceptance are changing. Communities want transparency, local value, water accountability, ratepayer protection and confidence that development will not overwhelm their infrastructure.

For the organizations accountable for mission-critical delivery, this creates a new commercial reality. The projects most likely to move forward will be those that connect public-permission risk to power planning, procurement strategy and field readiness from the start.

Capital, demand and technology remain necessary. They are no longer sufficient.

Permission is becoming a critical path item.

Delivery perspective

The underlying issue is not simply opposition to data centers. It is coordination failure.

Owners, developers, utilities, contractors, procurement teams, public agencies and communities are often working from different information, different incentives and different timelines. In a market where one local decision can alter a multi-billion-dollar program, that fragmentation becomes expensive.

Mission-critical construction now needs a more connected operating view. Power availability, permitting risk, procurement status, vendor signals, logistics milestones and field readiness need to be understood together, before they become delays.

The data center boom will continue. The question is which projects can convert ambition into buildable capacity.